CONTENTS

- 1. Accounting Fraud Investigation | Overview of the Case Strengthening Sanctions for Audit Obstruction and the Content of the Amendment

- - Principal Amendments Announced by the Financial Supervisory Service

- 2. Accounting Fraud Investigation | The Structure of the Audit Obstruction the Financial Authorities Took Issue With

- - Refusal to Submit Materials

- - Submission of False Materials

- - Non-compliance with Audit Committee Requests

- 3. Accounting Fraud Investigation | Why Audit Obstruction Is Assessed as a Serious Violation

- - The Accounting Supervision System

- - The Process of Detecting Accounting Fraud

- - Nullification of the Accounting Supervision Function

- 4. Accounting Fraud Investigation | Risks Companies Should Confirm and Response Strategies

- - Principal Risks

- - The Corporate Attorney's Strategy

1. Accounting Fraud Investigation | Overview of the Case Strengthening Sanctions for Audit Obstruction and the Content of the Amendment

In the course of an accounting fraud investigation, the accounting records, internal documents, contracts, and financial data held by the company become the primary subjects of examination.

Accordingly, the timely submission of the materials requested by the supervisory authority or the external auditor can be regarded as a precondition for the accounting supervision system to function normally.

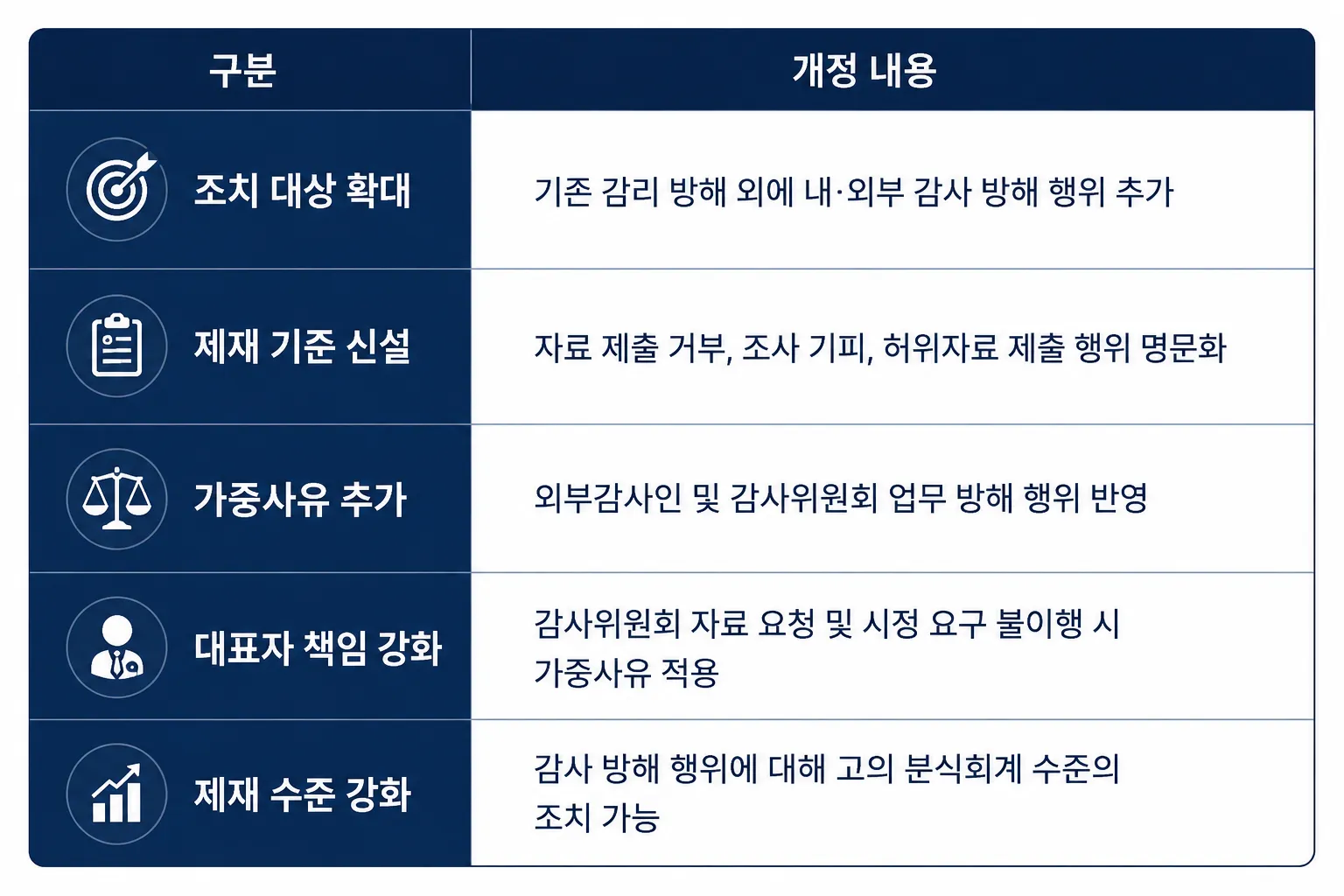

Through its 2025 amendment to the Detailed Enforcement Rules on External Audits and Accounting, the Financial Supervisory Service included not only existing acts of obstructing review but also acts of obstructing external audits and acts of obstructing internal audits among the subjects of sanctions.

This is interpreted as a measure intended to regulate more strictly any attempt to nullify the investigation itself during an accounting fraud investigation.

The core of this amendment is that, independently of whether accounting fraud has actually been detected, the act of obstructing an accounting fraud investigation is itself assessed as an independent risk factor.

Principal Amendments Announced by the Financial Supervisory Service

Principal Amendments Announced by the Financial Supervisory Service

Previously, the focus was often placed on whether an actual violation of accounting standards or an occurrence of accounting fraud had taken place.

This amendment, however, draws attention to the point that refusing to submit materials or submitting false materials during an accounting fraud investigation can likewise impair the effectiveness of the accounting supervision system.

In particular, the financial authorities take the view that the cooperation of the company under investigation is indispensable for the accounting supervision system, which proceeds from internal audit to external audit and then to accounting review, to function normally.

Accordingly, where a company repeatedly fails to submit the materials necessary for the investigation or submits materials that differ from the facts, this may be assessed as an act of obstructing the supervisory function itself, independently of whether there has been an actual violation of accounting standards.

This amendment is aimed not only at sanctions following the detection of accounting fraud but also at strengthening the proactive management framework for securing the effectiveness of accounting fraud investigations, and it can be assessed as a case demonstrating that the duty of companies to cooperate with investigations and the importance of operating an internal control system have grown still further.

2. Accounting Fraud Investigation | The Structure of the Audit Obstruction the Financial Authorities Took Issue With

What deserves attention in this case of amending the regulations on accounting fraud investigations is that it is not a case in which actual accounting fraud was detected.

The financial authorities determined that, even at a stage before a violation of accounting standards has been confirmed, the act of obstructing an audit or investigation can itself undermine the accounting supervision system.

An accounting fraud investigation is a procedure for confirming whether a company's financial statements have been prepared in accordance with accounting standards.

In this process, the Financial Supervisory Service, the external auditor, and the audit committee secure the relevant materials and verify the facts. However, where materials are not submitted or false materials are submitted, the investigation itself is difficult to conduct normally.

Category | Description |

|---|---|

Refusal to Submit Materials | Repeatedly refusing or delaying compliance with requests to submit materials |

Obstruction of or Evasion of the Investigation | Obstructing the investigation, inspection, or verification procedures |

Submission of False Materials | Submitting materials that differ from the facts |

Non-compliance with Audit Requests | Failing to comply with the requests of the auditor or the audit committee |

Failure to Implement Corrective Requests | Failing to implement requests to correct accounting treatment |

The financial authorities took the view that, if such situations recur, the function of detecting accounting fraud could in effect be nullified, and through this amendment they added acts of obstructing audits as grounds for aggravated sanctions.

Refusal to Submit Materials

In an accounting fraud investigation, various materials, such as financial statements, accounting books, contracts, vouchers, and tax invoices, become subjects of examination.

The Financial Supervisory Service or the external auditor reviews the substance of transactions and the appropriateness of the accounting treatment on the basis of those materials.

Accordingly, where materials are not submitted, it may become difficult to determine whether there has been a violation of accounting standards.

This amendment included, among the subjects of measures, the act of refusing, obstructing, or evading a request to submit materials or a request for inspection three or more times without justifiable cause.

Submission of False Materials

An accounting fraud investigation is a procedure for confirming the facts on the premise of the materials submitted.

Accordingly, where false materials are submitted, there is a risk that the supervisory authority will proceed with its determination on the basis of distorted information.

Where a company submits materials that make a nonexistent transaction appear to be a normal transaction, or that state the timing and amount of a transaction differently, this may affect the very outcome of the investigation.

The reason the financial authorities specified the submission of false materials as an act of obstructing audits is that it can undermine the reliability of the accounting supervision system.

Non-compliance with Audit Committee Requests

This amendment included among the grounds for aggravation not only acts that obstruct the external auditor but also acts that obstruct the performance of duties by the auditor or the audit committee.

The audit committee performs the role of examining the appropriateness of the company's accounting treatment and the status of internal control operations.

Accordingly, where a representative director or members of management refuse, without justifiable reason, requests for the provision of materials, requests for the provision of information, or requests for cost support, the internal audit function may become difficult to operate normally.

The financial authorities determined that such acts could, as a result, impair the effectiveness of accounting fraud investigations.

3. Accounting Fraud Investigation | Why Audit Obstruction Is Assessed as a Serious Violation

What is most notable in the amendment to the regulations on accounting fraud investigations is that it made it possible to impose sanctions on acts of obstructing audits at a level comparable to that for intentional accounting fraud.

Given that audit obstruction is itself assessed as a serious violation even where a violation of accounting standards has not been confirmed, companies need to examine the significance of this point.

Behind the financial authorities' introduction of such a measure lies the determination that the effectiveness of the accounting supervision system must be secured.

The Accounting Supervision System

For an accounting fraud investigation to be effective, internal audit, external audit, and the financial authorities' accounting review must function in an integrated manner.

The reason the financial authorities assess audit obstruction as serious is also related to these characteristics of the accounting supervision system.

The domestic accounting supervision system currently operates as follows.

Category | Role |

|---|---|

Internal Audit | Examination of accounting treatment and internal controls |

External Audit | Verification of the appropriateness of financial statements |

Accounting Review | Investigation of whether accounting standards have been violated |

Financial Services Commission | Final determination of sanctions and administrative measures |

Because each stage operates in connection with the others in this way, where materials cannot be secured at a particular stage or the audit procedure is obstructed, the effectiveness of the accounting supervision system as a whole may decline.

The Process of Detecting Accounting Fraud

An accounting fraud investigation often begins when anomalous signs are discovered during the external audit process or the analysis of disclosure materials.

To confirm the appropriateness of accounting treatment, the financial authorities review not only financial statements but also various materials, such as contracts, accounting books, tax invoices, and fund-flow data.

Principal Materials Reviewed | Purpose of Review |

|---|---|

Financial Statements | Confirmation of the results of accounting treatment |

Accounting Books | Verification of transaction records |

Contracts | Confirmation of the actual existence of transactions |

Tax Invoices | Confirmation of sales and purchase facts |

Fund Records | Analysis of transaction flows |

In this process, the substance of transactions and the appropriateness of accounting treatment can be confirmed only when materials are submitted properly.

Nullification of the Accounting Supervision Function

The reason the financial authorities take issue with acts of obstructing audits is that the function of detecting accounting fraud itself may fail to operate properly.

Where a refusal to submit materials, the submission of false materials, or obstruction of an investigation occurs, the supervisory authority finds it difficult to confirm the necessary facts.

In particular, the submission of false materials is assessed as still more serious in that it creates a risk that determinations will be made on the basis of distorted information.

In the end, acts of obstructing audits became a principal background to this amendment of the regulations, in that they can impair the effectiveness of the accounting supervision system, which proceeds from internal audit to external audit and then to accounting review.

4. Accounting Fraud Investigation | Risks Companies Should Confirm and Response Strategies

The amendment to the regulations on accounting fraud investigations shows that not only whether accounting standards have actually been violated but also whether the duty to cooperate during the investigation has been fulfilled can be an important factor in the determination.

Taking the view that the refusal to submit accounting records, the submission of false records, and acts of obstructing audits can impair the effectiveness of the accounting supervision system, the financial authorities reorganized the system in the direction of strengthening the related sanctions.

In particular, this case is significant in that not only the case in which accounting fraud is detected but also acts of obstruction that occur during the accounting fraud investigation itself can lead to separate legal risks.

From a company's standpoint, there is a need not only to examine response measures after an accounting review or external audit has begun but also to check whether the accounting-record management framework and internal control procedures are being operated appropriately in ordinary times.

Principal Risks

Category | Principal Content |

|---|---|

Designation of Auditor | A designated audit may apply for a certain period |

Sanctions on Officers | A recommendation to dismiss the representative director and the responsible officers, or a suspension from duties, is possible |

Criminal Risk | Possibility of an accusation of executives and employees to the prosecutors' office |

Management Risk | Decline in the trust of investors and business partners |

Internal Control Risk | Possible inclusion among subjects of additional supervision and examination |

A feature of this amendment is that, independently of whether accounting fraud is actually detected, the act of obstructing an audit can itself be grounds for sanctions.

Accordingly, a company needs to manage not only whether accounting standards have been violated but also whether the duty to cooperate during the investigation has been fulfilled.

In particular, where a refusal to submit materials, the submission of false materials, or non-compliance with audit committee requests is confirmed, liability may extend not only to the company but also to the representative director and the responsible officers.

The financial authorities also place importance on whether an environment in which the accounting supervision system can function normally has been established.

Accordingly, there is a need to examine the accounting-record retention procedures, the internal approval framework, and the audit response process, among others.

The Corporate Attorney's Strategy

▶ Review of legal issues arising during external auditor audit procedures, audit committee investigations, and Financial Supervisory Service reviews, and advisory on responses

▶ Advance risk analysis regarding whether accounting standards have been violated, the appropriateness of the preparation of financial statements, and the operational status of the internal accounting control system

▶ Responses to administrative sanction procedures, such as the designation of an auditor, the imposition of penalty surcharges and administrative fines, recommendations to dismiss officers, and suspensions from duties, and support in preparing written opinions

▶ Review of the scope of liability of the representative director, the chief financial officer (CFO), and accounting staff, and advisory on responses to criminal and administrative risks

▶ Compliance examination of the internal control system, the accounting-record retention framework, and the audit response process as a whole, and the presentation of improvement measures

Daeryun, the ninth-largest law firm in South Korea (based on 2025 value-added tax filings with the National Tax Service), supports companies in responding to legal risks related to accounting reviews, external audits, internal controls, and financial regulation, drawing on a systematic collaboration structure among specialists across multiple fields, including certified public accountants, attorneys experienced in financial matters, and attorneys handling corporate advisory work.

If you need to respond to such matters, we invite you to review, through the 🔗corporate attorney legal consultation booking, the procedures and direction of response suited to your company's current situation.